I’m writing this from Greece, taking a brief holiday with two of my children. It has been amazing to be away from the daily deluge of misery coming out of our elected Government in the UK, and spend some time outside looking in. Those who follow me on LinkedIn will know I’ve remained on top of economic news and am extremely concerned about where we are, which nobody in power seems to appreciate. But this blog isn’t about my holiday, or the wider economy, so let me zoom in a bit to telecoms.

There’s been a phenomenon since the Great Financial Crash in 2008 where interest rates were low or negligible called ‘buy and build’. You could borrow money in the low single-digits, buy a thriving business making 10-20% EBITDA margins, borrowing 8-12x EBITDA and pocket the difference. The business paid for itself essentially – you didn’t even need to repay the debt, just service the interest as it’d all come out in the wash when the amalgam was itself “flipped”. This leverage enabled the equity value to grow in a geared way. Others came at it from the other end, with PE funding levering up businesses with double-digit loan notes, but extra-ordinary returns for the equity holders, on paper at least.

Many of the largest operators in our sector have grown this way. Some have integrated the businesses they’ve bought to make a proper bigger business. Others have just strapped on mediocrity without integrating anything – but who cares when you have leverage. In fact you can even ruin some of the businesses you buy and still be ahead. It really is an easy win and there’s some huge ego’s built on what they think is clever.

We have some buy and builds amongst our customer base, some where our customers were the initial platform company, and far more where our customer has been acquired. The latter are hard work – I can think of several who are aggressive and used to committing fraud to get what they want. I’ve told the tale before of one who wanted us to put our customer out of business by permitting them to commit fraud, and went on to try to do it anyway by extorting end-users to change the underlying supplier. I’m not a fan of them, their dirty way of doing business, and the entirely misplaced self-adoration they exude at a senior level. But I digress…

I like financial engineering. Many of you know I cut my teeth in financial services and am still very active. We’ve flirted with buy-and-build before but, to be perfectly honest, a few things held me back. One was the risk of integration although we did that pretty well I think with Sipcentric and Birchills – two acquisitions we made in 2019 under our own steam – and the other was building a dependence on external parties (PE or debt providers) who would build protections in for themselves the net result being our equity holders took on excessive downside risk. Add to that the general dearth of opportunity – many great businesses doing their own great things, but not really integratable into a larger whole properly – and the risk-reward has never stacked up for me. In a recent interview I was described as having “no corporate ambition” which I suppose is one interpretation of the above although I have to say irked me. No doubt some of the egos active in buy-and-build, who have never started and run a business for 30 years but consider themselves God’s gift to commerce, found it amusing.

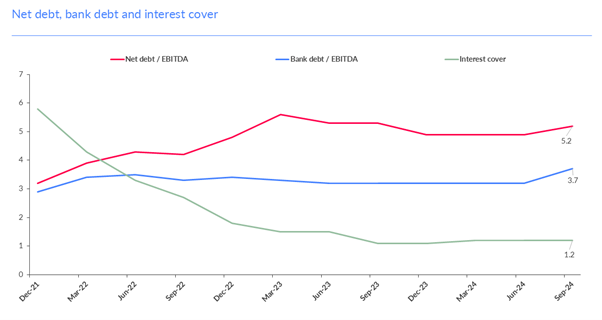

So what is the point I’m getting to? I mentioned a few years ago how in some of these businesses that I track, their ability to service even the interest on their debt was waning. Many in the market track interest cover which is profit before tax (EBIT) as a multiple of interest payments. Megabyte this week put out a paper warning that across the sector interest cover was at just 1.2x, down from 6 over the last three years, leaving little room for error. Personally, I don’t like interest cover because it assumes that EBIT is actually usable. I much prefer to look at EBITDA, since it better approximates cash generated. On an EBITDA basis, while EBITDA is generally higher than EBIT, interest cover for some is already below 1, i.e. the business is making less usable/cash profit than the cost of servicing their debt. That assumes they make EBITDA at all which in some cases is a bit of a stretch. Those who do, look pretty tight and I suspect some egos may be getting checked soon – they’re essentially running a Ponzi scheme where servicing existing debt requires taking on more. As Megabyte highlights, their net debt is already at an average of 5.2x EBITDA, i.e. they need to devote 100% of EBITDA to debt repayment for over five years, assuming they don’t have to borrow more to keep the Ponzi going. As Bernie Madoff found out, Ponzi schemes do not last forever.

Source: Megabyte

As I look forward, and avoiding getting into politics, I see profitability compressed due to inflating costs which cannot be passed on, I see growth (the obvious antidote) being pretty tough, tax in whatever form rising (which while not always affecting EBITDA, drains cash from the business) and then we get into the real kicker. The Government makes a bit of a song and dance about the Bank of England cutting interest rates, yet the bond markets show we have the highest cost of borrowing in the developed world at the Government level, and inflation is rising. In a 1970s style stagflation environment we’re going to see the double whammy of rising interest rates and stagnant growth. How do some of these businesses look when their credit line rolls over and needs renewing at 2x or more the interest rate? On average they’re insolvent which means some of the outliers are going to be in extreme distress.

At the far edges it gets pretty scary. A few operators have negative EBITDA in excess of their interest costs, i.e. they simply cannot service their debt. Another has interest payments of nearly 10x its EBITDA and it is little surprise they were acquired – could we consider them failed? Next on the list is a very large regional operator whose interest costs are 87% of EBITDA – a cover of just 1.15x – and another even larger who has recently refinanced but its latest accounts (2023) show 1.16x cover – 86% of EBITDA servicing debt. At those kinds of (remarkably similar) levels, a 1.2-1.3% increase renders their debt unserviceable without immediate refinancing/restructuring. Yet another, the largest of the cohort, looked healthy at the operating company level (with 222x cover) but in classic PE style had pushed leverage to the holding company which only had cover of 0.59x – it required a £60m cash injection annually just to service debt. I use past tense because it strangely has also restructured a few times since – first selling assets to reduce debt, then finding a strategic partner for scale and stability – which feels like a distressed company rescue to me. For those remaining, even if base rates don’t change, deteriorating credit conditions or ratings could see any premium on refinancing trigger distress as well, and we have no idea what banking covenants lurk which could do so sooner. I have confidence that in some cases changed leadership recognises and are addressing the risk, but I have absolute belief in others not having a clue and still pursuing the “growth-at-any-cost” strategy until circumstance hits them round the face.

This isn’t meant to depress you or stoke any flames and in fact is an opportunity. Simwood is largely debt free (our interest cover is 12.5x but we have treasury assets amply sufficient to clear our debt on demand anyway), a good number of our competitors are low debt too, so a number of us are well placed for the waters we’re heading into, regardless of size. Our mutual customers are in the main tightly run businesses too. Sure, the CEOs don’t strut around thinking how clever they are, but they can pay bills when they fall due and deliver certain service to end users. If end-user SMEs were to appreciate some of this, and make decisions based on it, that would be a net win for the sensible and competent, and a positive step for our industry. I’m also curious how the regulator isn’t overtly dialled into this – the supplier of last resort process requires a willing and able supplier to step in and is meant for exceptions, not BaU.

I’m reminded of the florist who was “cut-off” in the run up to Mother’s Day by one of these arseholes. It still upsets me. In that case it was vindictive and utterly unforgivable, but what happens when they can’t service their debt and service is affected? That is a florist who is out of business, in fact that is tens or hundreds of thousands of businesses who are potentially out of business. They can’t migrate when their service is down and their supplier has ceased trading. They can now however and I would strongly encourage our customers to guide them on that path, whether our customer is a sensible buy-and-build or a tightly run small ship. Small isn’t a disability – survivability deserves a premium regardless of size.