Call me a saddo, but one of the nice things about the gap around Christmas and New Year is that I get some quiet time. In years gone by (many many years ago) that lead to brand new entire APIs, but nowadays involves me running esoteric queries and spotting trends.

I’ve been looking at three things this time, porting automation, porting charges and nuisance calls. Somewhat unrelated you might think; so did I.

Porting automation has been a huge focus for us in 2025 but one of the things that is often overlooked is that we’re not writing against a well-formed central API. Quite the opposite, we’re exposing well formed APIs to our customers and trying to make some sense out of the human randomness and often chaos of the UK’s porting process. There is a written “process” which involves humans emailing (or faxing) spreadsheets to each other and the whole thing relies on those humans replying to the right email, attaching the right spreadsheet, with the right boxes filled in in the right way, having not completely bastardised the format because they won’t buy Excel. You’d be astonished how hard this is, but add in BPOs who do not give a toss or companies who go out of their way to frustrate the process and it quickly unwinds.

Our automations take advantage of any bots which exist on the other side and leverage humans doing the right thing in the right way, when and where such a phenomenon exists. Humans take Some customers use our APIs and webhooks very extensively and have fairly robust processes on their own side for data validation and ensuring cleanliness. Others don’t! It is little surprise therefore that we have several accounts who over 2025 as a whole have achieved 100% of ports being processed without human intervention, and several who have achieved 0%. Chasing ports, arguing about responses and submitting poor data, all preclude us being able to let the robots do the magic even if they otherwise could, and propensity to doso also varies by customer. account of vagaries and other human behaviour really well, but automating it is hard. There are two key factors which drive our success here, and ultimately the rate of ‘porting automation credits’ we can apply to an account:

Our customer

Some customers use our APIs and webhooks very extensively and have fairly robust processes on their own side for data validation and ensuring cleanliness. Others don’t! It is little surprise therefore that we have several accounts who over 2025 as a whole have achieved 100% of ports being processed without human intervention, and several who have achieved 0%. Chasing ports, arguing about responses and submitting poor data, all preclude us being able to let the robots do the magic even if they otherwise could, and propensity to do so also varies by customer.

Of course, 100% is not the norm and across the entire universe of accounts we see just over 33% processed automatically, with several large accounts clustered in the 55% region. Considering stats are dragged down by those who underperform (including a large residential provider at 0% for ‘reasons’), and 100% is not realistically achievable at huge volume, we consider 55% about where the watermark currently lies. Higher than this – well done you, keep at it. Lower than this – there’s probably some tweaks you can make to raise the bar and lower your costs. Our team can probably give you pointers on why they’re having to intervene.

The LCP

It is no secret that our industry has different levels of competence, different levels of ‘with it’ness and dramatically different levels of ‘give a toss’. There are those who seek to do things consistently and efficiently, and there are those who do their damndest to not do things at all. Which LCP is on the other side of your port is going to be the biggest driver of automation success, once the basics are down. Looking over 2025, excluding the smaller volume losing providers the results are quite interesting. You can consider these a score of consistency and process uniformity, as there are providers in there with efficient robots, but who still manage to require heavy intervention. There are others in there we know will do everything they can to frustrate the process and in some case demonstrate a lack of any kind of diligence in their business more widely. I won’t draw my own conclusions but if you’ve been about this industry long enough you no doubt will.

| LCP | Auto % |

| BT Group | 36.1 |

| Wightfibre | 24.6 |

| Gamma Telecom | 22.0 |

| Sky | 19.2 |

| KCOM Group | 17.1 |

| Vodafone | 17.8 |

| Voicehost (IPEX) | 13.3 |

| Virgin Media | 9.3 |

| Talktalk Communications | 8.9 |

| Voiceflex (IPEX) | 8.5 |

| AQL | 8.3 |

| Colt | 7.0 |

| Magrathea Telecoms | 5.8 |

| Wavecrest Networks | 1.0 |

| Voxbone Sa | 0.0 |

| GCI Network Solutions | 0.0 |

This of course doesn’t show the volume of orders. While top LCPs are generally clustered at the top, there are some large donor providers around the middle and bottom quartile. Again, you’ll know who.

Correlation with Nuisance Calls?

I hadn’t intended writing about this but the thread of lack of process and lack of diligence piqued my interest. Now I must stress correlation is not causation, and these are unrelated data sets. But… one could make an argument that a lack of diligence in one area of a business could indicate a lack of diligence in another, or that a provider who goes out of their way to frustrate a customer’s right to change service provider, might also be inclined to take on ‘wrong-uns’. Below is a list of Range Holders where we have blocked more than 100k calls via our nuisance call algorithms, together with their percentage of the total. Those who appear on the porting list are shaded grey for comparison but remember these lists are ordered inversely – someone with low porting consistency will be at the bottom of the first sheet, someone who is sending lots of nuisance calls will be at the top of the second.

One critical consideration here is market share. You’d expect a provider with 40% of the market like BT to rank highly, maybe pushing 40%, and thus only accounting for 9.5% of nuisance calls is quite good. Conversely, you wouldn’t expect a provider with no discernable market share to represent over a quarter. I won’t name and shame here but we’ve run the numbers (nuisance calls vs market share) and, combined with an excess of virtue signalling from the operator concerned, lead to our post “Beware: the Fox is in the Hen House“.

| Range Holder | Calls blocked | Percentage of total |

| Vodafone (All) | 4,342,692 | 27.7 |

| Voxbone SA | 4,128,973 | 26.3 |

| DIDWW Ireland Limited | 1,994,019 | 12.7 |

| BT | 1,485,348 | 9.5 |

| Twilio Ireland Limited | 1,065,617 | 6.8 |

| AQL (All) | 934,908 | 6.0 |

| Gamma Telecom Holdings Limited | 915,511 | 5.8 |

| Tismi BV | 844,145 | 5.4 |

| WAVECREST NETWORKS LIMITED | 539,312 | 3.4 |

| GCI Network Solutions Limited | 515,905 | 3.3 |

| Core Telecom Limited | 479,149 | 3.1 |

| Belgacom International Carrier Services SA | 349,839 | 2.2 |

| Net-Work Internet Ltd | 258,324 | 1.6 |

| TAP GATEWAY LTD | 168,549 | 1.1 |

| Hutchison 3G UK Ltd | 165,935 | 1.1 |

| IP Voice Networks Ltd | 156,443 | 1.0 |

| TELNYX UK LIMITED | 137,999 | 0.9 |

| API Telecom Limited | 136,279 | 0.9 |

| Magrathea Telecommunications Limited | 135,669 | 0.9 |

| Others | 1,229,150 | 7.8 |

| 15,700,719 |

Of course, while the Range Holder may have suballocated the number, they might not be the current provider. They could have lax KYC but numbers may have been ported away, could be spoofed, or they may simply not be a network themselves to originate traffic. Which interconnect calls came into Simwood on, excluding numbers ported to us, therefore has some significance. Those stats paint an even clearer picture, but they’re eyes only for those attending our webinar on nuisance calls!

Common causation or correlation? You decide.

Export charges

There was a theme in our survey responses that we’d put prices up. In fact our prices have fallen dramatically in real-terms having not been increased for years. We have however introduced new charges, such as one for exports, which I understand might be perceived as an increase. However, from our perspective this was offset by the automation discount, such that on aggregate we effectively reduced porting charges. I said you’d have to trust me but have run the numbers for December.

It turns out that we gave an automation saving 1.24x our charges for exports. It varies by account of course with net importers seeing huge savings, and net exporters (rightly in my view) carrying the cost of the work incurred. There are some accounts with low percentage automations which derive less of a saving but overall 24% is not to be sneezed at. Ironically, some of the largest savings are on those accounts who perceived an increase, so I’d urge you to run your own numbers!

Thankfully, despite or perhaps because of this unilateral discounting, our porting volumes are are +78% this December compared to last. It seems you like the combination of ports being processed as fast as inhumanly possible, rich APIs, and a 75% discount where we don’t need to get involved. Keep them coming!

Human involvement

Lastly, for all the automation in the world, in an industry process as broken as porting, you need some ninjas. We’ve been able to grow volumes by letting the computers take the strain and leaving the ninjas more time to persuade those who like to abuse the process or coach the simply incompetent. They’re an essential ingredient whose contribution will hopefully fall as a percentage over time, but the value of which will continue to exponentially grow.

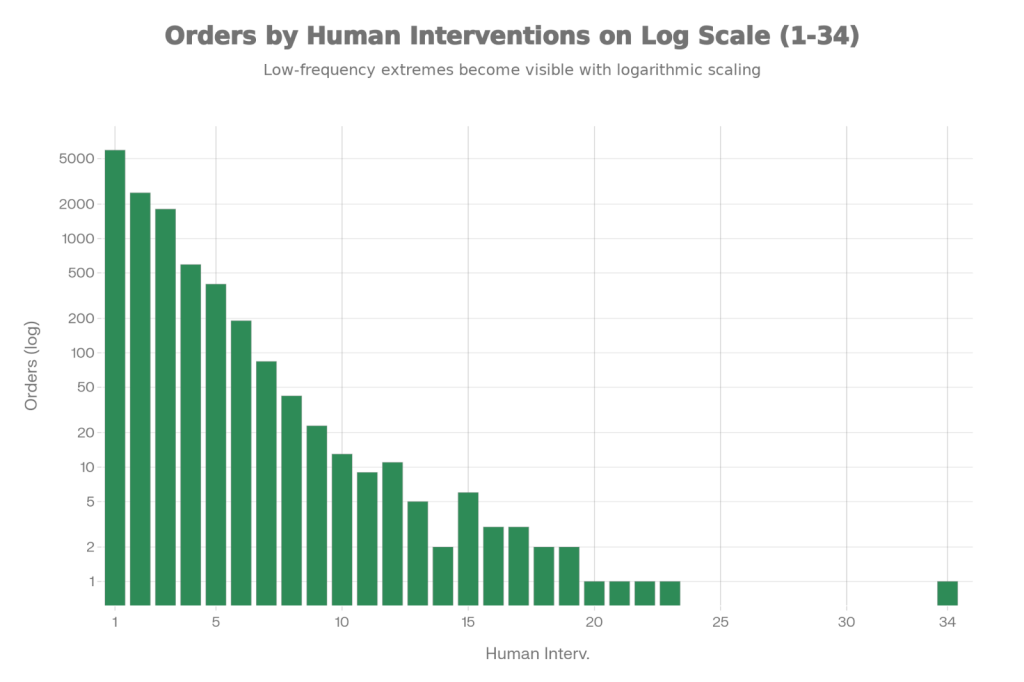

One interesting metric is how many times per order they have had to intervene. An intervention could be answering the phone to explain and justify to a customer why we haven’t had a response in the 3 seconds since they submitted the order – yes, really – or it could be sitting on hold to a BPO for two hours, and anything in between. What is fascinating is the number of orders which need multiple interventions. Most are 1-3, but there’s one in there with 34! Little wonder porting remains a loss-leader for us.

Because I couldn’t resist, here is that same data grouped by losing provider. I’ve excluded all the low volume LCPs for clarity but you can see on average, each port requires multiple interventions but how many varies by losing provider. There are some excluded providers with a low volume of orders but much higher intervention counts than anything shown! These figures include those which sailed through automation as well.

| LCP | Interventions per order |

| Colt | 3.71 |

| Magrathea Telecoms | 2.26 |

| Vodafone group | 2.14 |

| TalkTalk Communications | 1.82 |

| Virgin Media | 1.82 |

| Gamma Telecom Holdings | 1.69 |

| Sky UK (incl. Business) | 1.34 |

| BT | 1.23 |

I’ll let you be the judge of whether the worst players here are foul play, incompetence or something else. You might want to compare them to some of the other tables, remembering some are inverted!

Underlying data is available for any Regulator who wishes to dig a little deeper!

That’s enough indulgent geekery for me for one day. Have a wonderful New Year!